Ch4: Classification#

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import statsmodels.api as sm

from ISLP import load_data

from ISLP.models import (ModelSpec as MS,

summarize)

sns.set_theme()

%matplotlib inline

from ISLP import confusion_table

from sklearn.discriminant_analysis import \

(LinearDiscriminantAnalysis as LDA,

QuadraticDiscriminantAnalysis as QDA)

from sklearn.naive_bayes import GaussianNB

from sklearn.neighbors import KNeighborsClassifier

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LogisticRegression

Conceptual#

Q1.#

Starting with (4.2):

Multiply both sides by:

To get:

Rearranging the terms:

Factoring out \(e^{\beta_0 + \beta_1 X}\) and dividing both sides by the remainder:

We get (4.3) which is what we set out to prove.

Q2.#

Taking the \( log \) of both sides:

To maximize the value of the function above over all k we only need to consider terms that vary with k:

The term \( -\frac{x^2}{2\sigma^2} \) is constant across all values of k so we can ignore it and the remaining 3 terms are what we have to consider:

Q3.#

This question is similar to the previous question except for the assumption that \(\sigma_1^2 = ... = \sigma_K^2\) which we don’t apply here:

Following the same steps used in the above question, taking the log and considering only terms that vary with k:

We can see that the discriminant function takes the form:

Which is quadratic in x.

Q4.#

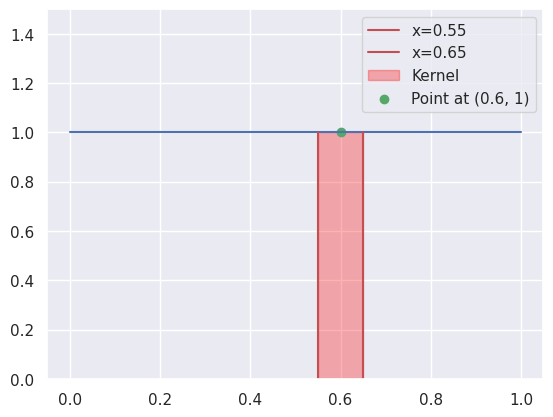

(a) To answer this question we can imagine a kernel of width 0.1 sweeping along the X-axis from 0 to 1, where the area of the kernel around a point X corresponds to the fraction of available observations we use to make a prediction for the response of test observation X.

The following figure just helps us visualise what we mean to do. And intuitivly the result should be close to 10% since it stays 10% for all points in the range [0.05, 0.95] and slightly decreases outside that range.

fig, ax = plt.subplots()

ax.set_ylim([0, 1.5])

# Plot the horizontal line

ax.plot([0, 1], [1, 1], c='b')

# Add vertical red lines using ax.plot (absolute coordinates)

ax.plot([0.55, 0.55], [0, 1], c='r', label='x=0.55') # Line from y=0 to y=1

ax.plot([0.65, 0.65], [0, 1], c='r', label='x=0.65') # Line from y=0 to y=1

# Shade the area between the two vertical lines

ax.axvspan(0.55, 0.65, 0, 1/ax.get_ylim()[1], color='red', alpha=0.3, label='Kernel')

ax.scatter(0.6, 1, c='g', label='Point at (0.6, 1)')

ax.legend()

plt.show()

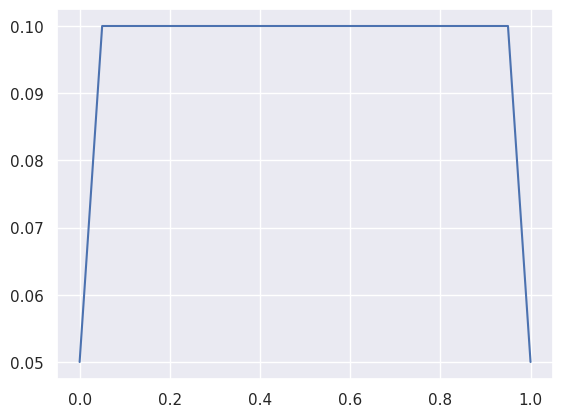

within = 0.1

lim = within/2

obs = np.linspace(0, 1, 1001)

used_obs = np.array([])

for i in obs:

left = i - lim

if left < 0:

left = 0

right = i + lim

if right > 1:

right = 1

# print(f'[{left:.2f}, {right:.2f}]')

used_obs = np.append(used_obs, right - left)

plt.plot(obs, used_obs);

used_obs.mean()

0.09745254745254749

We can see that on average, the fraction of available observations we use to make the prediction is 9.75%.

(b) Extending the idea above from 2 dimensions (p = 1) to 3 dimensions (p = 2).

within = 0.10

lim = within/2

obs = np.arange(0, 1, 0.01)

p = 2

used_obs = []

for n in range(p):

used_obs_dim = []

for i in obs:

minimum = i - lim

if minimum < 0:

minimum = 0

max = i + lim

if max > 1:

max = 1

# print(f'[{min:.2f}, {max:.2f}]')

used_obs_dim.append(max - minimum)

used_obs.append(used_obs_dim)

used_obs = np.array(used_obs)

import operator

from functools import reduce

grid = np.meshgrid(*used_obs, indexing="ij")

result = reduce(operator.mul, grid)

result.mean()

0.009506250000000008

We can see that on average we use 0.95% of the available observations to make the prediction.

(c)

Similar to what we did above we just extend the same ideas to a 101 dimensions (p = 100). Creating the grid for the data would be troublesome so we’ll just use the fact that from every dimension we use 9.75% of the data like so.

0.0975 ** 2

0.00950625

We can see that we get the same result we calculated above for p = 2.

0.0975 ** 100

7.951728986183188e-102

As we can see the value is so miniscule that we’re practically using almost 0% of the available observations to make a prediction.

(d) Looking at our answers from (a)-(c) we can see that the more predictors we use while considering a non-parametric method like KNN, the less test observations are used to make the prediction, since data points become very sparse in higher dimensions.

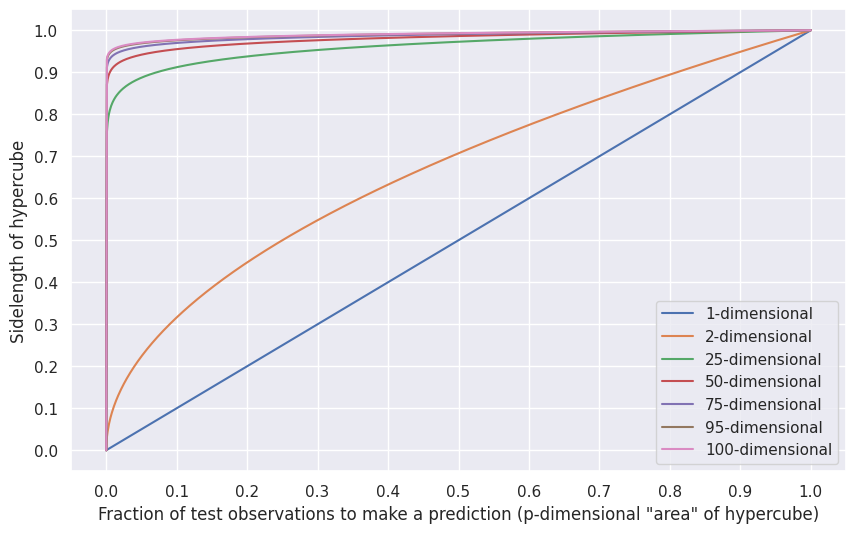

(e) To find the sidelength of the hypercube that contains 10% of the testing observations we just need to find the sidelength of a p-dimensional hypercube that has a p-dimensional “area” of 0.10.

for \(p = 1\) that’d be:

for \(p = 2\) that’d be:

np.power(0.10, 1/2)

0.31622776601683794

for \( p = 100 \):

np.power(0.10, 1/100)

0.9772372209558108

We can see that for large values of p the sidelength of the hypercube gets so big to the point where it’s close to 1 but only 10% of test observations fall within the hypercube, which is a testament to how sparse data in high dimensional space gets.

I’ll create a plot to capture that relation for various values of p:

fig, ax = plt.subplots(figsize=(10, 6))

for p in [1, 2, 25, 50, 75, 95, 100]:

x = np.linspace(0, 1, 1001)

ax.plot(x, np.power(x, 1/p), label=f'{p}-dimensional')

ax.set_xticks(np.arange(0, 1.1, 0.1))

ax.set_yticks(np.arange(0, 1.1, 0.1))

ax.set_xlabel('Fraction of test observations to make a prediction (p-dimensional "area" of hypercube)')

ax.set_ylabel('Sidelength of hypercube')

ax.legend();

Q5.#

(a) We expect QDA to perform better on the training set than LDA due to it being a more flexible model, however we expect LDA to perform better on the test set since it’d have less bias due to the Bayes decision boundary being linear.

(b) QDA would perform better on both the training and test sets, because here the increase in variance from using a more flexible model (QDA) is offset by a decrease in bias due to the Bayes decision boundary being non-linear.

(c) We expect it to improve, as the additional incurred cost in variance from choosing a more flexible classifer (QDA over LDA) is offset by the large sample size.

(d) False. Because the resulting increase in variance from using a more flexible model isn’t offset by any decrease in bias since the Bayes decision boundary is linear hence LDA would have a better test error rate than QDA.

Q6.#

(a) We can simply do that using the formula:

b0 = -6

b1 = 0.05

b2 = 1

def predict(Hours, GPA):

numerator = np.exp(b0 + b1 * Hours + b2 * GPA)

denominator = 1 + np.exp(b0 + b1 * Hours + b2 * GPA)

return numerator / denominator

predict(40, 3.5)

0.37754066879814546

The student has a probability of 37.75% to get an A in that class.

(b) To find the amount of time he’s required to study to make his probability of getting an A 50% we just plug 50% for \(p\) and solve for \(Hours\):

p = 0.5

GPA = 3.5

Hours = (np.log(p/(1-p)) - b0 - b2 * GPA)/b1

Hours

50.0

We see that he needs to study 10 more hours (for a total of 50 hours) to increase his probability of getting an A to 50%.

Q7.#

From the given information we can see that the assumptions are the same as those for LDA, namely X follows a normal distribution with constant variance across the classes.

Using Bayes’ theorem with the assumption that \(f_k(x)\) is normally distributed:

def f(x, mean, variance, prior):

return prior * (1/np.sqrt(2 * np.pi * variance)) * np.exp((-1/(2*variance)) * (x - mean)**2)

f(4, 10, 36, 0.8)/(f(4, 0, 36, 0.2) + f(4, 10, 36, 0.8))

0.7518524532975261

We can see that a company that had a percentage profit of X = 4 last year has a probability of 75.19% to issue a dividend this year.

Q8.#

We should still use logistic regression because it’s very likely that the KNN (with K=1) classifier overfit to the data resulting in a training error rate of around 0% and a test error rate of 36% which is higher than LR’s 30% test error rate.

Q9.#

(a)

0.37/(1 + 0.37)

0.27007299270072993

27% of people with an odds of 0.37 of defaulting on their credit card will default.

(b)

0.16/(1 - 0.16)

0.1904761904761905

She has an odds of 0.19 that she’ll default.

Q10.#

Starting with:

And considering the case for \(p = 1\), where the means \(\mu_1, ..., \mu_K\) and variance \(\sigma^2\) are scalars:

Where

Q11.#

Starting with:

And considering the case for \(p > 1\), where the means \(\mu_1, ..., \mu_K\) are p-dimensional vectors, and \(\Sigma_1, ..., \Sigma_k\) are \(p \times p\) covariance matrices (A multivariate normal distribution):

Where

And

Note: The notation above is just a way of indexing, indicating that for example \(b_{kj}\) is the \(j\text{th}\) component of \((\mathbf{\mu_k}^T \mathbf{\Sigma_k}^{-1} - \mathbf{\mu_K}^T \mathbf{\Sigma_K}^{-1})\).

Q12.#

(a)

The log odds of orange versus apple in my model is \(\hat{\beta}_0 + \hat{\beta}_1 x\)

(b)

The log odds of orange versus apple in our friend’s model is \((\hat{\alpha}_{orange0} - \hat{\alpha}_{apple0}) + (\hat{\alpha}_{orange1} - \hat{\alpha}_{apple1}) x\)

(c) The given coefficients for our model:

By equating the log odds results from both models:

By equating the log odds results from both models:

From this we can see that infinitely many solutions exist, basically any two values with a difference equal to the estimated \(\hat\beta\) coefficient would suffice.

Where \(c_0, c_1\) are constants. We can set these constants to 0 to eliminate redundancy and obtain the simplest case of:

(d) Note: There seems to be a mistake in the given coefficients of the question where it gives the coefficients for orange twice but not for apple so I’ll assume the second set of coefficients is apple’s.

Using the same equations from above:

beta0 = 1.2 - 3

beta1 = -2 - 0.6

beta0, beta1

(-1.8, -2.6)

The coefficient estimates for our model are

(e) I expect them to agree every time since the two models are equivalent and it’s only a different coding of the same underlying logistic regression model.

Applied#

Q13.#

weekly = load_data('Weekly')

weekly.head()

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | Direction | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 1990 | 0.816 | 1.572 | -3.936 | -0.229 | -3.484 | 0.154976 | -0.270 | Down |

| 1 | 1990 | -0.270 | 0.816 | 1.572 | -3.936 | -0.229 | 0.148574 | -2.576 | Down |

| 2 | 1990 | -2.576 | -0.270 | 0.816 | 1.572 | -3.936 | 0.159837 | 3.514 | Up |

| 3 | 1990 | 3.514 | -2.576 | -0.270 | 0.816 | 1.572 | 0.161630 | 0.712 | Up |

| 4 | 1990 | 0.712 | 3.514 | -2.576 | -0.270 | 0.816 | 0.153728 | 1.178 | Up |

(a)

weekly.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1089 entries, 0 to 1088

Data columns (total 9 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Year 1089 non-null int64

1 Lag1 1089 non-null float64

2 Lag2 1089 non-null float64

3 Lag3 1089 non-null float64

4 Lag4 1089 non-null float64

5 Lag5 1089 non-null float64

6 Volume 1089 non-null float64

7 Today 1089 non-null float64

8 Direction 1089 non-null category

dtypes: category(1), float64(7), int64(1)

memory usage: 69.4 KB

weekly.describe()

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | |

|---|---|---|---|---|---|---|---|---|

| count | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 |

| mean | 2000.048669 | 0.150585 | 0.151079 | 0.147205 | 0.145818 | 0.139893 | 1.574618 | 0.149899 |

| std | 6.033182 | 2.357013 | 2.357254 | 2.360502 | 2.360279 | 2.361285 | 1.686636 | 2.356927 |

| min | 1990.000000 | -18.195000 | -18.195000 | -18.195000 | -18.195000 | -18.195000 | 0.087465 | -18.195000 |

| 25% | 1995.000000 | -1.154000 | -1.154000 | -1.158000 | -1.158000 | -1.166000 | 0.332022 | -1.154000 |

| 50% | 2000.000000 | 0.241000 | 0.241000 | 0.241000 | 0.238000 | 0.234000 | 1.002680 | 0.241000 |

| 75% | 2005.000000 | 1.405000 | 1.409000 | 1.409000 | 1.409000 | 1.405000 | 2.053727 | 1.405000 |

| max | 2010.000000 | 12.026000 | 12.026000 | 12.026000 | 12.026000 | 12.026000 | 9.328214 | 12.026000 |

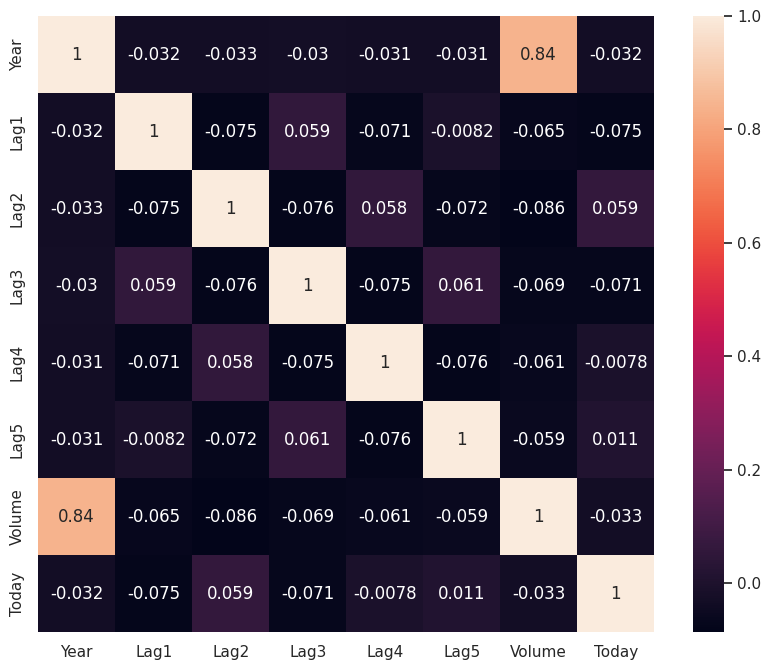

numeric_cols = weekly.select_dtypes(include=np.number).columns

weekly_numeric = weekly[numeric_cols]

plt.figure(figsize=(10, 8))

sns.heatmap(weekly_numeric.corr(), annot=True, square=True)

<Axes: >

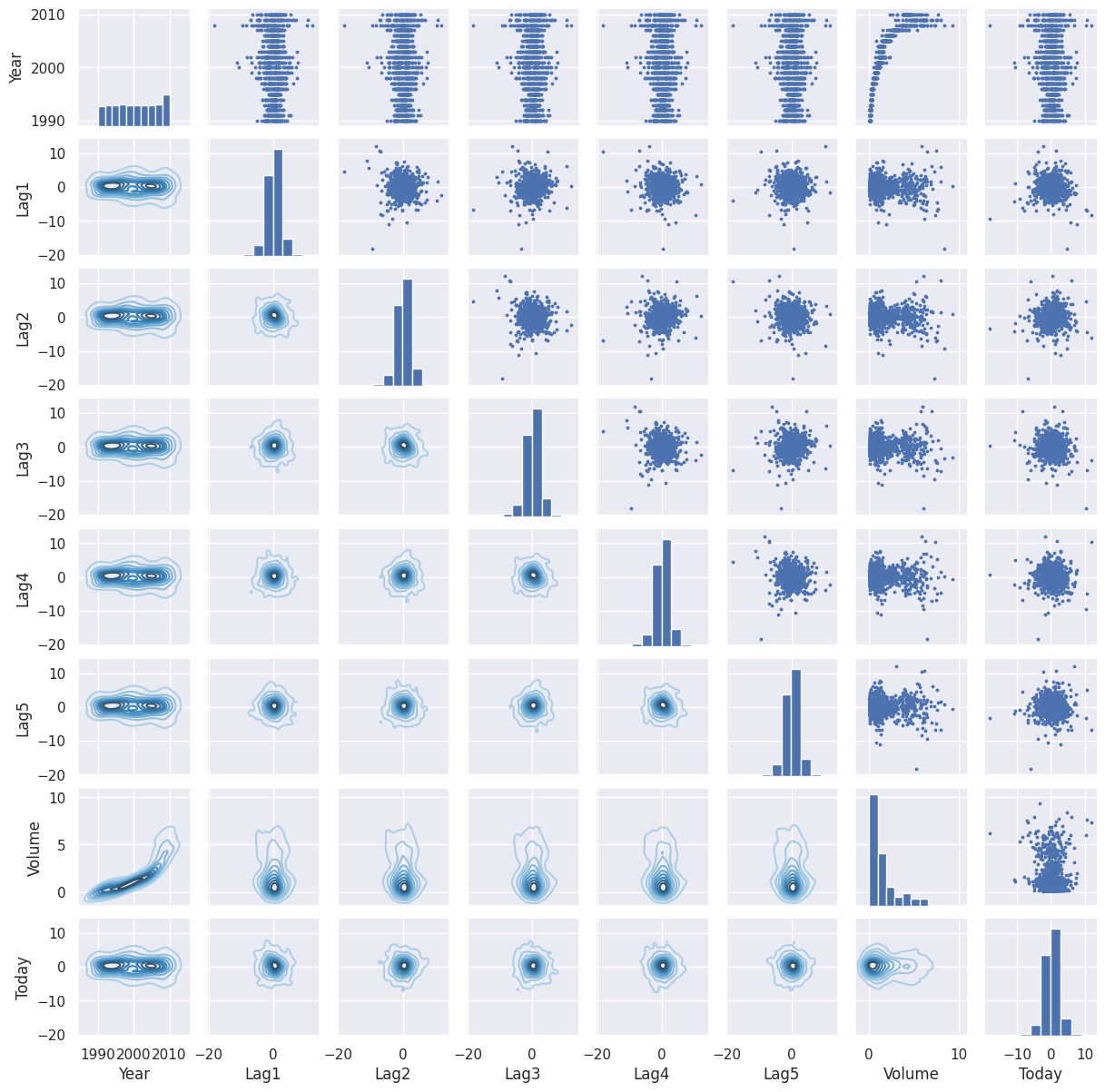

g = sns.PairGrid(weekly)

g.map_upper(plt.scatter, s=3)

g.map_diag(plt.hist)

g.map_lower(sns.kdeplot, cmap="Blues_d")

g.figure.set_size_inches(12, 12)

From the plots above we can see that there aren’t any prominant relationships in the data aside from Volume growing with Year.

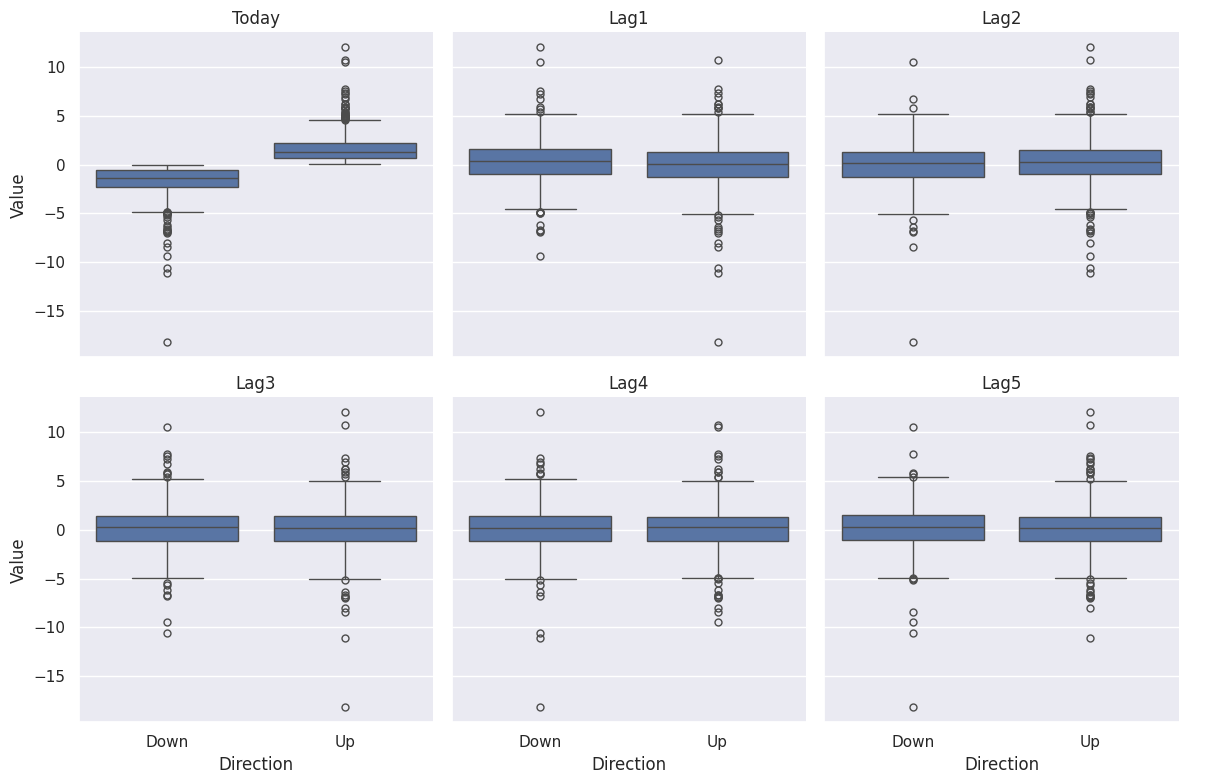

# Melt DataFrame to long format

weekly_melt = weekly.melt(id_vars=['Direction'],

value_vars=['Today', 'Lag1', 'Lag2', 'Lag3', 'Lag4', 'Lag5'],

var_name='Lag',

value_name='Value')

# Create box plots for each Lag variable

g = sns.catplot(x='Direction', y='Value', col='Lag',

data=weekly_melt, kind='box',

col_wrap=3, height=4, aspect=1)

g.set_titles("{col_name}")

plt.show()

(b)

vars = weekly.columns.drop(['Today', 'Year', 'Direction'])

design = MS(vars)

X = design.fit_transform(weekly)

y = weekly['Direction'] == 'Up'

glm = sm.GLM(y,

X,

family=sm.families.Binomial())

results = glm.fit()

summarize(results)

| coef | std err | z | P>|z| | |

|---|---|---|---|---|

| intercept | 0.2669 | 0.086 | 3.106 | 0.002 |

| Lag1 | -0.0413 | 0.026 | -1.563 | 0.118 |

| Lag2 | 0.0584 | 0.027 | 2.175 | 0.030 |

| Lag3 | -0.0161 | 0.027 | -0.602 | 0.547 |

| Lag4 | -0.0278 | 0.026 | -1.050 | 0.294 |

| Lag5 | -0.0145 | 0.026 | -0.549 | 0.583 |

| Volume | -0.0227 | 0.037 | -0.616 | 0.538 |

Only Lag2 seems to be statistically significant at a confidence level of 5%.

(c)

probs = results.predict()

probs

array([0.60862494, 0.60103144, 0.58756995, ..., 0.57972297, 0.55091703,

0.52212163])

labels = np.array(['Down']*1089)

labels[probs>0.5] = "Up"

np.unique(labels, return_counts=True)

(array(['Down', 'Up'], dtype='<U4'), array([102, 987]))

np.unique(weekly['Direction'], return_counts=True)

(array(['Down', 'Up'], dtype=object), array([484, 605]))

confusion_table(labels, weekly['Direction'])

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 54 | 48 |

| Up | 430 | 557 |

(54+ 557)/1089, 605/1089

(0.5610651974288338, 0.5555555555555556)

The fraction of correct predictions is 56.1% which is 6.1% better than random guessing and 0.55% better than the null classifer (always predicting Up).

We can also see from the confusion matrix that our model made 430 type I errors and 48 type II errors.

(d)

weekly90_08 = weekly[weekly['Year'] <= 2008]

weekly90_08.describe()

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | |

|---|---|---|---|---|---|---|---|---|

| count | 985.000000 | 985.000000 | 985.000000 | 985.000000 | 985.000000 | 985.000000 | 985.000000 | 985.000000 |

| mean | 1999.050761 | 0.124501 | 0.127820 | 0.122884 | 0.122227 | 0.120976 | 1.205973 | 0.130535 |

| std | 5.457286 | 2.269346 | 2.269069 | 2.272617 | 2.272625 | 2.274273 | 1.258204 | 2.279069 |

| min | 1990.000000 | -18.195000 | -18.195000 | -18.195000 | -18.195000 | -18.195000 | 0.087465 | -18.195000 |

| 25% | 1994.000000 | -1.154000 | -1.147000 | -1.154000 | -1.154000 | -1.154000 | 0.307337 | -1.154000 |

| 50% | 1999.000000 | 0.231000 | 0.234000 | 0.231000 | 0.230000 | 0.230000 | 0.804848 | 0.231000 |

| 75% | 2004.000000 | 1.334000 | 1.337000 | 1.337000 | 1.337000 | 1.337000 | 1.515846 | 1.337000 |

| max | 2008.000000 | 12.026000 | 12.026000 | 12.026000 | 12.026000 | 12.026000 | 9.328214 | 12.026000 |

weekly09_10 = weekly[weekly['Year'] > 2008]

weekly09_10.describe()

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | |

|---|---|---|---|---|---|---|---|---|

| count | 104.000000 | 104.000000 | 104.000000 | 104.000000 | 104.000000 | 104.000000 | 104.000000 | 104.000000 |

| mean | 2009.500000 | 0.397635 | 0.371365 | 0.377548 | 0.369250 | 0.319058 | 5.066105 | 0.333298 |

| std | 0.502421 | 3.068538 | 3.074725 | 3.075192 | 3.073895 | 3.073650 | 1.147652 | 3.003296 |

| min | 2009.000000 | -7.035000 | -7.035000 | -7.035000 | -7.035000 | -7.035000 | 2.390427 | -7.035000 |

| 25% | 2009.000000 | -1.060750 | -1.214250 | -1.214250 | -1.214250 | -1.323250 | 4.234228 | -1.060750 |

| 50% | 2009.500000 | 0.522000 | 0.461500 | 0.522000 | 0.461500 | 0.437000 | 4.850717 | 0.461500 |

| 75% | 2010.000000 | 2.239250 | 2.239250 | 2.239250 | 2.239250 | 2.204250 | 5.793837 | 2.204250 |

| max | 2010.000000 | 10.707000 | 10.707000 | 10.707000 | 10.707000 | 10.707000 | 7.963276 | 10.707000 |

design = MS(['Lag2'])

X = design.fit_transform(weekly90_08)

y = weekly90_08['Direction'] == 'Up'

glm = sm.GLM(y,

X,

family=sm.families.Binomial())

results = glm.fit()

summarize(results)

| coef | std err | z | P>|z| | |

|---|---|---|---|---|

| intercept | 0.2033 | 0.064 | 3.162 | 0.002 |

| Lag2 | 0.0581 | 0.029 | 2.024 | 0.043 |

X = design.fit_transform(weekly09_10)

probs = results.predict(X)

probs[:10]

985 0.526129

986 0.644736

987 0.486216

988 0.485200

989 0.519767

990 0.540125

991 0.623348

992 0.480993

993 0.451220

994 0.484881

dtype: float64

len(weekly09_10)

104

labels = np.array(['Down']*104)

labels[probs>0.5] = "Up"

confusion_table(labels, weekly09_10['Direction'])

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 9 | 5 |

| Up | 34 | 56 |

(9+56)/104, 61/104

(0.625, 0.5865384615384616)

The fraction of correct predictions is 62.5% which is 12.5% better than random guessing and 3.8% better than the null classifer (always predicting Up).

(e) Since we’ll end up using the same code to fit all the models on the same data I’ll create a function to make that easier:

def fit_and_test(model):

design = MS(['Lag2'], intercept=False)

X_train = design.fit_transform(weekly90_08)

X_test = design.fit_transform(weekly09_10)

L_train = weekly90_08['Direction']

L_test = weekly09_10['Direction']

mdl = model

mdl = mdl.fit(X_train, L_train)

pred = mdl.predict(X_test)

return confusion_table(pred, L_test)

Using LDA:

lda = LDA(store_covariance=True)

fit_and_test(lda)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 9 | 5 |

| Up | 34 | 56 |

(9+56)/(104)

0.625

The fraction of correct predictions is 62.5% which is 12.5% better than random guessing. We can also see that this resulted in the exact same confusion matrix as the Logistic Regression.

(f) Using QDA:

qda = QDA(store_covariance=True)

fit_and_test(qda)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 0 | 0 |

| Up | 43 | 61 |

61/104

0.5865384615384616

We can see that the QDA model here is equivalent to always predicting Up hence it has the same error rate as the null classifer .

(g) Using KNN with K = 1:

knn = KNeighborsClassifier(n_neighbors=1)

fit_and_test(knn)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 22 | 32 |

| Up | 21 | 29 |

(22+29)/104

0.49038461538461536

The fraction of correct predictions is 49% which is even worse than random guessing here and much worse than the null classifer.

(h) Using Naive Bayes:

nb = GaussianNB()

fit_and_test(nb)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 0 | 0 |

| Up | 43 | 61 |

We can see that the Naive Bayes model here is equivalent to always predicting Up hence it has the same error rate as the null classifer and QDA.

(i) LDA and Logistic Regression seem to provide the best predictions with an accuracy of 62.5%.

(j) We’ll try a few different combinations of predictors, transformations, and interactions for each of the methods.

We’ll start by making a slight modification to the function we defined above.

def fit_and_test(modelspec, model):

"""

Takes a ModelSpec for the weekly dataset and a model and trains it on data from 1990 to 2008,

then tests it on the data from 2009 to 2010 and returns the fraction of correct predictions and a confusion

matrix for the given model and testing.

"""

design = modelspec

X_train = design.fit_transform(weekly90_08)

X_test = design.fit_transform(weekly09_10)

L_train = weekly90_08['Direction']

L_test = weekly09_10['Direction']

mdl = model

mdl = mdl.fit(X_train, L_train)

pred = mdl.predict(X_test)

conf_mat = confusion_table(pred, L_test)

print(model.__repr__())

print(f'fraction of correct predictions: {(conf_mat.iloc[0, 0] + conf_mat.iloc[1, 1])/len(pred):.3f}')

return conf_mat

modelspec = MS(['Lag2', 'Lag5', 'Lag3', ('Lag2', 'Lag5'), ('Lag5', 'Lag3')])

fit_and_test(modelspec, LogisticRegression())

LogisticRegression()

fraction of correct predictions: 0.606

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 9 | 7 |

| Up | 34 | 54 |

modelspec = MS(['Lag2', 'Volume', ('Lag2', 'Volume')])

fit_and_test(modelspec, LogisticRegression())

LogisticRegression()

fraction of correct predictions: 0.529

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 19 | 25 |

| Up | 24 | 36 |

modelspec = MS(['Lag2', 'Lag5', 'Lag3', ('Lag2', 'Lag5'), ('Lag5', 'Lag3')], intercept=False)

for model in [LDA(), QDA(), GaussianNB()]:

print(fit_and_test(modelspec, model))

print()

LinearDiscriminantAnalysis()

fraction of correct predictions: 0.615

Truth Down Up

Predicted

Down 9 6

Up 34 55

QuadraticDiscriminantAnalysis()

fraction of correct predictions: 0.538

Truth Down Up

Predicted

Down 11 16

Up 32 45

GaussianNB()

fraction of correct predictions: 0.529

Truth Down Up

Predicted

Down 10 16

Up 33 45

modelspec = MS(['Lag1', 'Lag2', 'Lag5', ('Lag1', 'Lag2'), ('Lag5', 'Lag2')], intercept=False)

for model in [LDA(), QDA(), GaussianNB()]:

print(fit_and_test(modelspec, model))

print()

LinearDiscriminantAnalysis()

fraction of correct predictions: 0.567

Truth Down Up

Predicted

Down 8 10

Up 35 51

QuadraticDiscriminantAnalysis()

fraction of correct predictions: 0.538

Truth Down Up

Predicted

Down 12 17

Up 31 44

GaussianNB()

fraction of correct predictions: 0.529

Truth Down Up

Predicted

Down 8 14

Up 35 47

Looking at all the combinations of variables and models above we can see that not many get close to LDA and LR’s accuracy score of 62.5% when fit on Lag2. Closest score we had was LDA fit on Lag2, Lag5, Lag3, (Lag2 x Lag5), (Lag5 x Lag3) with an accuracy of 61.5%.

modelspec = MS(['Lag2'], intercept=False)

for k in range(1, 31):

print(fit_and_test(modelspec, KNeighborsClassifier(n_neighbors=k)))

print()

KNeighborsClassifier(n_neighbors=1)

fraction of correct predictions: 0.490

Truth Down Up

Predicted

Down 22 32

Up 21 29

KNeighborsClassifier(n_neighbors=2)

fraction of correct predictions: 0.462

Truth Down Up

Predicted

Down 31 44

Up 12 17

KNeighborsClassifier(n_neighbors=3)

fraction of correct predictions: 0.558

Truth Down Up

Predicted

Down 16 19

Up 27 42

KNeighborsClassifier(n_neighbors=4)

fraction of correct predictions: 0.577

Truth Down Up

Predicted

Down 26 27

Up 17 34

KNeighborsClassifier()

fraction of correct predictions: 0.538

Truth Down Up

Predicted

Down 16 21

Up 27 40

KNeighborsClassifier(n_neighbors=6)

fraction of correct predictions: 0.510

Truth Down Up

Predicted

Down 20 28

Up 23 33

KNeighborsClassifier(n_neighbors=7)

fraction of correct predictions: 0.548

Truth Down Up

Predicted

Down 16 20

Up 27 41

KNeighborsClassifier(n_neighbors=8)

fraction of correct predictions: 0.548

Truth Down Up

Predicted

Down 21 25

Up 22 36

KNeighborsClassifier(n_neighbors=9)

fraction of correct predictions: 0.558

Truth Down Up

Predicted

Down 17 20

Up 26 41

KNeighborsClassifier(n_neighbors=10)

fraction of correct predictions: 0.567

Truth Down Up

Predicted

Down 22 24

Up 21 37

KNeighborsClassifier(n_neighbors=11)

fraction of correct predictions: 0.567

Truth Down Up

Predicted

Down 19 21

Up 24 40

KNeighborsClassifier(n_neighbors=12)

fraction of correct predictions: 0.567

Truth Down Up

Predicted

Down 23 25

Up 20 36

KNeighborsClassifier(n_neighbors=13)

fraction of correct predictions: 0.596

Truth Down Up

Predicted

Down 20 19

Up 23 42

KNeighborsClassifier(n_neighbors=14)

fraction of correct predictions: 0.567

Truth Down Up

Predicted

Down 21 23

Up 22 38

KNeighborsClassifier(n_neighbors=15)

fraction of correct predictions: 0.587

Truth Down Up

Predicted

Down 20 20

Up 23 41

KNeighborsClassifier(n_neighbors=16)

fraction of correct predictions: 0.577

Truth Down Up

Predicted

Down 21 22

Up 22 39

KNeighborsClassifier(n_neighbors=17)

fraction of correct predictions: 0.596

Truth Down Up

Predicted

Down 21 20

Up 22 41

KNeighborsClassifier(n_neighbors=18)

fraction of correct predictions: 0.587

Truth Down Up

Predicted

Down 22 22

Up 21 39

KNeighborsClassifier(n_neighbors=19)

fraction of correct predictions: 0.567

Truth Down Up

Predicted

Down 19 21

Up 24 40

KNeighborsClassifier(n_neighbors=20)

fraction of correct predictions: 0.596

Truth Down Up

Predicted

Down 23 22

Up 20 39

KNeighborsClassifier(n_neighbors=21)

fraction of correct predictions: 0.558

Truth Down Up

Predicted

Down 19 22

Up 24 39

KNeighborsClassifier(n_neighbors=22)

fraction of correct predictions: 0.596

Truth Down Up

Predicted

Down 23 22

Up 20 39

KNeighborsClassifier(n_neighbors=23)

fraction of correct predictions: 0.567

Truth Down Up

Predicted

Down 20 22

Up 23 39

KNeighborsClassifier(n_neighbors=24)

fraction of correct predictions: 0.558

Truth Down Up

Predicted

Down 22 25

Up 21 36

KNeighborsClassifier(n_neighbors=25)

fraction of correct predictions: 0.548

Truth Down Up

Predicted

Down 19 23

Up 24 38

KNeighborsClassifier(n_neighbors=26)

fraction of correct predictions: 0.538

Truth Down Up

Predicted

Down 23 28

Up 20 33

KNeighborsClassifier(n_neighbors=27)

fraction of correct predictions: 0.529

Truth Down Up

Predicted

Down 18 24

Up 25 37

KNeighborsClassifier(n_neighbors=28)

fraction of correct predictions: 0.529

Truth Down Up

Predicted

Down 21 27

Up 22 34

KNeighborsClassifier(n_neighbors=29)

fraction of correct predictions: 0.548

Truth Down Up

Predicted

Down 19 23

Up 24 38

KNeighborsClassifier(n_neighbors=30)

fraction of correct predictions: 0.529

Truth Down Up

Predicted

Down 21 27

Up 22 34

Trying the KNN classifier using the Lag2 variable and neighbors from 1 to 30, we can see that it yielded the highest accuracy of 59.6% for values of K = 13, 17, 20, 22.

Q14.#

auto = load_data('Auto')

auto.head()

| mpg | cylinders | displacement | horsepower | weight | acceleration | year | origin | |

|---|---|---|---|---|---|---|---|---|

| name | ||||||||

| chevrolet chevelle malibu | 18.0 | 8 | 307.0 | 130 | 3504 | 12.0 | 70 | 1 |

| buick skylark 320 | 15.0 | 8 | 350.0 | 165 | 3693 | 11.5 | 70 | 1 |

| plymouth satellite | 18.0 | 8 | 318.0 | 150 | 3436 | 11.0 | 70 | 1 |

| amc rebel sst | 16.0 | 8 | 304.0 | 150 | 3433 | 12.0 | 70 | 1 |

| ford torino | 17.0 | 8 | 302.0 | 140 | 3449 | 10.5 | 70 | 1 |

auto.info()

<class 'pandas.core.frame.DataFrame'>

Index: 392 entries, chevrolet chevelle malibu to chevy s-10

Data columns (total 8 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 mpg 392 non-null float64

1 cylinders 392 non-null int64

2 displacement 392 non-null float64

3 horsepower 392 non-null int64

4 weight 392 non-null int64

5 acceleration 392 non-null float64

6 year 392 non-null int64

7 origin 392 non-null int64

dtypes: float64(3), int64(5)

memory usage: 27.6+ KB

auto.describe()

| mpg | cylinders | displacement | horsepower | weight | acceleration | year | origin | |

|---|---|---|---|---|---|---|---|---|

| count | 392.000000 | 392.000000 | 392.000000 | 392.000000 | 392.000000 | 392.000000 | 392.000000 | 392.000000 |

| mean | 23.445918 | 5.471939 | 194.411990 | 104.469388 | 2977.584184 | 15.541327 | 75.979592 | 1.576531 |

| std | 7.805007 | 1.705783 | 104.644004 | 38.491160 | 849.402560 | 2.758864 | 3.683737 | 0.805518 |

| min | 9.000000 | 3.000000 | 68.000000 | 46.000000 | 1613.000000 | 8.000000 | 70.000000 | 1.000000 |

| 25% | 17.000000 | 4.000000 | 105.000000 | 75.000000 | 2225.250000 | 13.775000 | 73.000000 | 1.000000 |

| 50% | 22.750000 | 4.000000 | 151.000000 | 93.500000 | 2803.500000 | 15.500000 | 76.000000 | 1.000000 |

| 75% | 29.000000 | 8.000000 | 275.750000 | 126.000000 | 3614.750000 | 17.025000 | 79.000000 | 2.000000 |

| max | 46.600000 | 8.000000 | 455.000000 | 230.000000 | 5140.000000 | 24.800000 | 82.000000 | 3.000000 |

(a)

mpg01 = auto['mpg'] > auto['mpg'].median()

mpg01

name

chevrolet chevelle malibu False

buick skylark 320 False

plymouth satellite False

amc rebel sst False

ford torino False

...

ford mustang gl True

vw pickup True

dodge rampage True

ford ranger True

chevy s-10 True

Name: mpg, Length: 392, dtype: bool

auto['mpg01'] = mpg01.astype(int)

auto.head()

| mpg | cylinders | displacement | horsepower | weight | acceleration | year | origin | mpg01 | |

|---|---|---|---|---|---|---|---|---|---|

| name | |||||||||

| chevrolet chevelle malibu | 18.0 | 8 | 307.0 | 130 | 3504 | 12.0 | 70 | 1 | 0 |

| buick skylark 320 | 15.0 | 8 | 350.0 | 165 | 3693 | 11.5 | 70 | 1 | 0 |

| plymouth satellite | 18.0 | 8 | 318.0 | 150 | 3436 | 11.0 | 70 | 1 | 0 |

| amc rebel sst | 16.0 | 8 | 304.0 | 150 | 3433 | 12.0 | 70 | 1 | 0 |

| ford torino | 17.0 | 8 | 302.0 | 140 | 3449 | 10.5 | 70 | 1 | 0 |

(b)

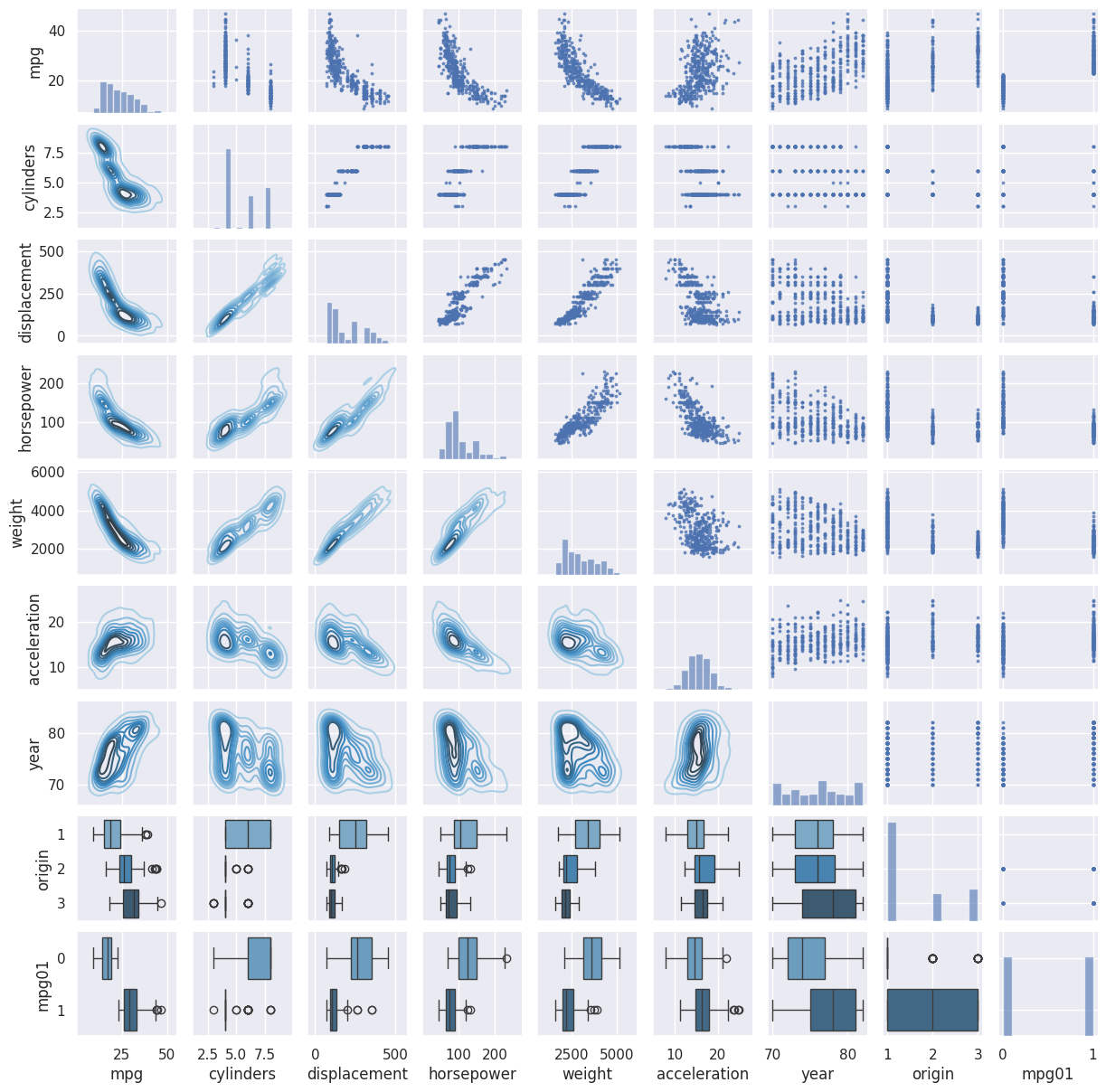

g = sns.PairGrid(auto)

g.map_upper(plt.scatter, s=3, alpha=0.7)

g.map_diag(plt.hist, alpha=0.6)

def lower_plots(x, y, **kwargs):

if y.name in ['mpg01', 'origin']:

num_colors_needed = y.nunique()

sns.boxplot(x=x, y=y, orient='h', hue=y, palette=sns.color_palette('Blues_d', n_colors=num_colors_needed), **kwargs) # Horizontal boxplot

else:

sns.kdeplot(x=x, y=y, cmap='Blues_d', **kwargs) # KDE plot

g.map_lower(lower_plots)

g.figure.set_size_inches(12, 12);

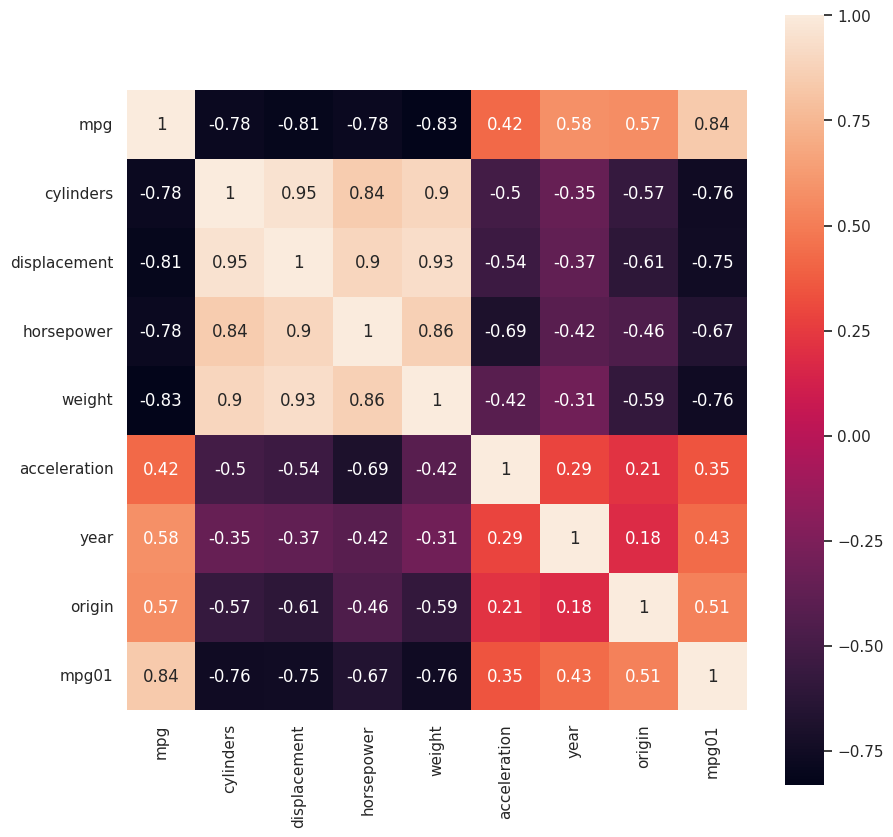

plt.figure(figsize=(10, 10))

sns.heatmap(auto.corr(), annot=True, square=True);

Looking at the heatmap and the plots above we can see that many of them have some sort of relationship with mpg01, the most useful for predicting mpg01 would likely be features like cylinders, displacement, horsepower, weight.

(c)

X = auto[['cylinders', 'displacement', 'horsepower', 'weight']]

y = auto['mpg01']

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.3, random_state=1)

(d) LDA:

lda = LDA()

lda.fit(X_train, y_train)

lda_pred = lda.predict(X_test)

lda_pred

array([1, 1, 1, 1, 1, 1, 1, 0, 1, 1, 0, 1, 0, 1, 1, 0, 1, 1, 0, 0, 1, 0,

0, 0, 0, 0, 1, 0, 0, 1, 0, 1, 0, 0, 0, 0, 0, 0, 1, 1, 0, 0, 1, 0,

0, 0, 0, 1, 0, 0, 0, 0, 1, 1, 1, 0, 1, 1, 1, 1, 0, 1, 1, 0, 0, 0,

1, 0, 1, 0, 1, 0, 0, 1, 1, 1, 0, 0, 0, 1, 0, 1, 1, 1, 0, 0, 1, 1,

1, 0, 1, 0, 0, 0, 0, 1, 0, 1, 0, 0, 1, 1, 0, 1, 1, 1, 0, 1, 0, 0,

1, 0, 1, 1, 0, 1, 0, 0])

Defining a quick function to get the error rate from a confusion matrix.

def get_error_rate(conf_mat):

return (conf_mat.iloc[0, 1] + conf_mat.iloc[1, 0])/conf_mat.sum().sum()

conf_mat = confusion_table(lda_pred, y_test)

conf_mat

| Truth | 0 | 1 |

|---|---|---|

| Predicted | ||

| 0 | 58 | 3 |

| 1 | 7 | 50 |

get_error_rate(conf_mat)

0.0847457627118644

The test error rate for LDA is 8.5%.

(e) QDA:

qda = QDA()

qda.fit(X_train, y_train)

qda_pred = qda.predict(X_test)

qda_pred

array([1, 1, 1, 1, 1, 1, 1, 0, 1, 1, 0, 1, 0, 1, 1, 0, 1, 1, 0, 0, 1, 0,

0, 0, 0, 0, 1, 0, 0, 1, 0, 1, 0, 0, 0, 0, 0, 0, 1, 1, 0, 0, 0, 0,

0, 0, 0, 1, 0, 0, 0, 0, 1, 1, 1, 0, 0, 0, 1, 1, 0, 1, 1, 0, 0, 0,

0, 0, 1, 0, 1, 0, 0, 1, 1, 1, 0, 0, 0, 1, 0, 1, 1, 1, 0, 0, 1, 1,

1, 0, 1, 0, 0, 0, 0, 0, 0, 1, 0, 0, 1, 1, 0, 1, 1, 1, 0, 1, 0, 0,

1, 0, 1, 1, 0, 1, 0, 0])

conf_mat = confusion_table(qda_pred, y_test)

conf_mat

| Truth | 0 | 1 |

|---|---|---|

| Predicted | ||

| 0 | 61 | 5 |

| 1 | 4 | 48 |

get_error_rate(conf_mat)

0.07627118644067797

The test error rate for QDA is 7.6%.

(f)

lr = LogisticRegression()

lr.fit(X_train, y_train)

lr_pred = lr.predict(X_test)

lr_pred

array([1, 1, 1, 1, 1, 1, 1, 0, 1, 1, 0, 1, 0, 1, 1, 0, 1, 1, 0, 0, 1, 0,

0, 0, 0, 0, 1, 0, 0, 1, 0, 1, 0, 0, 0, 0, 0, 0, 1, 1, 0, 0, 0, 0,

0, 0, 0, 1, 0, 0, 0, 0, 1, 1, 1, 0, 0, 1, 1, 1, 0, 1, 1, 0, 0, 0,

1, 0, 1, 0, 1, 0, 0, 1, 1, 1, 0, 0, 0, 1, 0, 1, 1, 1, 0, 0, 1, 1,

1, 0, 1, 0, 0, 0, 0, 0, 0, 1, 0, 0, 1, 1, 0, 1, 1, 1, 0, 1, 0, 0,

1, 1, 1, 1, 0, 1, 0, 0])

conf_mat = confusion_table(lr_pred, y_test)

conf_mat

| Truth | 0 | 1 |

|---|---|---|

| Predicted | ||

| 0 | 59 | 4 |

| 1 | 6 | 49 |

get_error_rate(conf_mat)

0.0847457627118644

The test error rate for Logistic Regression is 8.5%.

(g) Naive Bayes:

nb = GaussianNB()

nb.fit(X_train, y_train)

nb_pred = nb.predict(X_test)

nb_pred

array([1, 1, 1, 1, 1, 1, 1, 0, 1, 1, 0, 1, 0, 1, 1, 0, 1, 1, 0, 0, 1, 0,

0, 0, 0, 0, 1, 0, 0, 1, 0, 1, 0, 0, 0, 0, 0, 0, 1, 1, 0, 0, 0, 0,

0, 0, 0, 1, 0, 0, 0, 0, 1, 1, 1, 0, 0, 0, 1, 1, 0, 1, 1, 0, 0, 0,

1, 0, 1, 0, 1, 0, 0, 1, 1, 1, 0, 0, 0, 1, 0, 1, 1, 1, 0, 0, 1, 1,

1, 0, 1, 0, 0, 0, 0, 0, 0, 1, 0, 0, 1, 1, 0, 1, 1, 1, 0, 1, 0, 0,

1, 0, 1, 1, 0, 1, 0, 0])

conf_mat = confusion_table(nb_pred, y_test)

conf_mat

| Truth | 0 | 1 |

|---|---|---|

| Predicted | ||

| 0 | 60 | 5 |

| 1 | 5 | 48 |

get_error_rate(conf_mat)

0.0847457627118644

The test error rate for Naive Bayes is 8.5%.

(h) KNN:

For this we’ll use StandardScaler since KNN uses distances between points to make predictions.

scaler = StandardScaler(with_mean=True,

with_std=True,

copy=True)

X = auto[['cylinders', 'displacement', 'horsepower', 'weight']]

y = auto['mpg01']

X_std = scaler.fit_transform(X)

feature_std = pd.DataFrame(

X_std,

columns=X.columns);

feature_std.std()

cylinders 1.001278

displacement 1.001278

horsepower 1.001278

weight 1.001278

dtype: float64

X_train_std, X_test_std, y_train_std, y_test_std = train_test_split(np.asarray(feature_std), y, test_size=0.3,random_state=1)

error_rate = {}

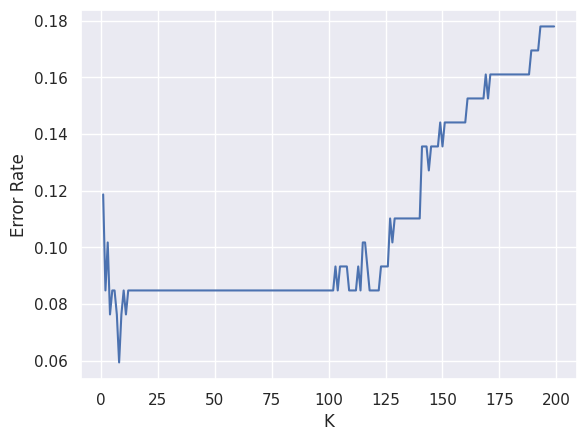

for k in range(1, 200):

knn = KNeighborsClassifier(n_neighbors=k)

knn.fit(X_train_std, y_train_std)

knn_pred = knn.predict(X_test_std)

conf_mat = confusion_table(knn_pred, y_test_std)

error_rate[k] = get_error_rate(conf_mat)

plt.plot(error_rate.keys(), error_rate.values())

plt.xlabel('K')

plt.ylabel('Error Rate');

k_min = min(error_rate, key=error_rate.get)

k_min, error_rate[k_min]

(8, 0.059322033898305086)

The best value for K in the KNN classifier for this dataset is 8 which resulted in the minimal error rate of 5.93%.

Q15.#

(a)

def Power():

""" Prints the result of raising 2 to the 3rd power """

print(2 ** 3)

Power()

8

(b)

def Power2(x, a):

""" Prints the result of raising x to the power a """

print(x ** a)

Power2(3, 8)

6561

(c)

Power2(10, 3)

Power2(8, 17)

Power2(131, 3)

1000

2251799813685248

2248091

(d)

def Power3(x, a):

""" returns the result of raising x to the power a """

result = x ** a

return result

(e)

x = np.arange(1, 11)

y = Power3(x, 2)

plt.plot (x, y)

plt.title('$f(x) = x^2$')

plt.xlabel('x-axis')

plt.ylabel('y-axis');

plt.xscale('log')

plt.yscale('log')

plt.plot (x, y)

plt.title('$f(x) = x^2$')

plt.xlabel('x-axis')

plt.ylabel('y-axis');

plt.xscale('log')

plt.plot (x, y)

plt.title('$f(x) = x^2$')

plt.xlabel('x-axis')

plt.ylabel('y-axis');

plt.yscale('log')

(f)

def PlotPower(x, a):

y = Power3(x, a)

plt.plot (x, y)

plt.title(f'$f(x) = x^{a}$')

plt.xlabel('x-axis')

plt.ylabel('y-axis');

PlotPower(np.arange(1, 11), 3)

Q16.#

The same as Q14.

boston = load_data('Boston')

boston.head()

| crim | zn | indus | chas | nox | rm | age | dis | rad | tax | ptratio | lstat | medv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.00632 | 18.0 | 2.31 | 0 | 0.538 | 6.575 | 65.2 | 4.0900 | 1 | 296 | 15.3 | 4.98 | 24.0 |

| 1 | 0.02731 | 0.0 | 7.07 | 0 | 0.469 | 6.421 | 78.9 | 4.9671 | 2 | 242 | 17.8 | 9.14 | 21.6 |

| 2 | 0.02729 | 0.0 | 7.07 | 0 | 0.469 | 7.185 | 61.1 | 4.9671 | 2 | 242 | 17.8 | 4.03 | 34.7 |

| 3 | 0.03237 | 0.0 | 2.18 | 0 | 0.458 | 6.998 | 45.8 | 6.0622 | 3 | 222 | 18.7 | 2.94 | 33.4 |

| 4 | 0.06905 | 0.0 | 2.18 | 0 | 0.458 | 7.147 | 54.2 | 6.0622 | 3 | 222 | 18.7 | 5.33 | 36.2 |

boston.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 506 entries, 0 to 505

Data columns (total 13 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 crim 506 non-null float64

1 zn 506 non-null float64

2 indus 506 non-null float64

3 chas 506 non-null int64

4 nox 506 non-null float64

5 rm 506 non-null float64

6 age 506 non-null float64

7 dis 506 non-null float64

8 rad 506 non-null int64

9 tax 506 non-null int64

10 ptratio 506 non-null float64

11 lstat 506 non-null float64

12 medv 506 non-null float64

dtypes: float64(10), int64(3)

memory usage: 51.5 KB

boston.describe()

| crim | zn | indus | chas | nox | rm | age | dis | rad | tax | ptratio | lstat | medv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 |

| mean | 3.613524 | 11.363636 | 11.136779 | 0.069170 | 0.554695 | 6.284634 | 68.574901 | 3.795043 | 9.549407 | 408.237154 | 18.455534 | 12.653063 | 22.532806 |

| std | 8.601545 | 23.322453 | 6.860353 | 0.253994 | 0.115878 | 0.702617 | 28.148861 | 2.105710 | 8.707259 | 168.537116 | 2.164946 | 7.141062 | 9.197104 |

| min | 0.006320 | 0.000000 | 0.460000 | 0.000000 | 0.385000 | 3.561000 | 2.900000 | 1.129600 | 1.000000 | 187.000000 | 12.600000 | 1.730000 | 5.000000 |

| 25% | 0.082045 | 0.000000 | 5.190000 | 0.000000 | 0.449000 | 5.885500 | 45.025000 | 2.100175 | 4.000000 | 279.000000 | 17.400000 | 6.950000 | 17.025000 |

| 50% | 0.256510 | 0.000000 | 9.690000 | 0.000000 | 0.538000 | 6.208500 | 77.500000 | 3.207450 | 5.000000 | 330.000000 | 19.050000 | 11.360000 | 21.200000 |

| 75% | 3.677083 | 12.500000 | 18.100000 | 0.000000 | 0.624000 | 6.623500 | 94.075000 | 5.188425 | 24.000000 | 666.000000 | 20.200000 | 16.955000 | 25.000000 |

| max | 88.976200 | 100.000000 | 27.740000 | 1.000000 | 0.871000 | 8.780000 | 100.000000 | 12.126500 | 24.000000 | 711.000000 | 22.000000 | 37.970000 | 50.000000 |

First we’ll create a variable crim01 which indicates whether the crime rate is below (0) or above (1) the median.

boston['crim01'] = (boston['crim'] > boston['crim'].median()).astype(int)

boston['crim01'].sample(5, random_state=1)

307 0

343 0

47 0

67 0

362 1

Name: crim01, dtype: int64

Now we’ll explore the data to see what features would be useful in predicting crim01.

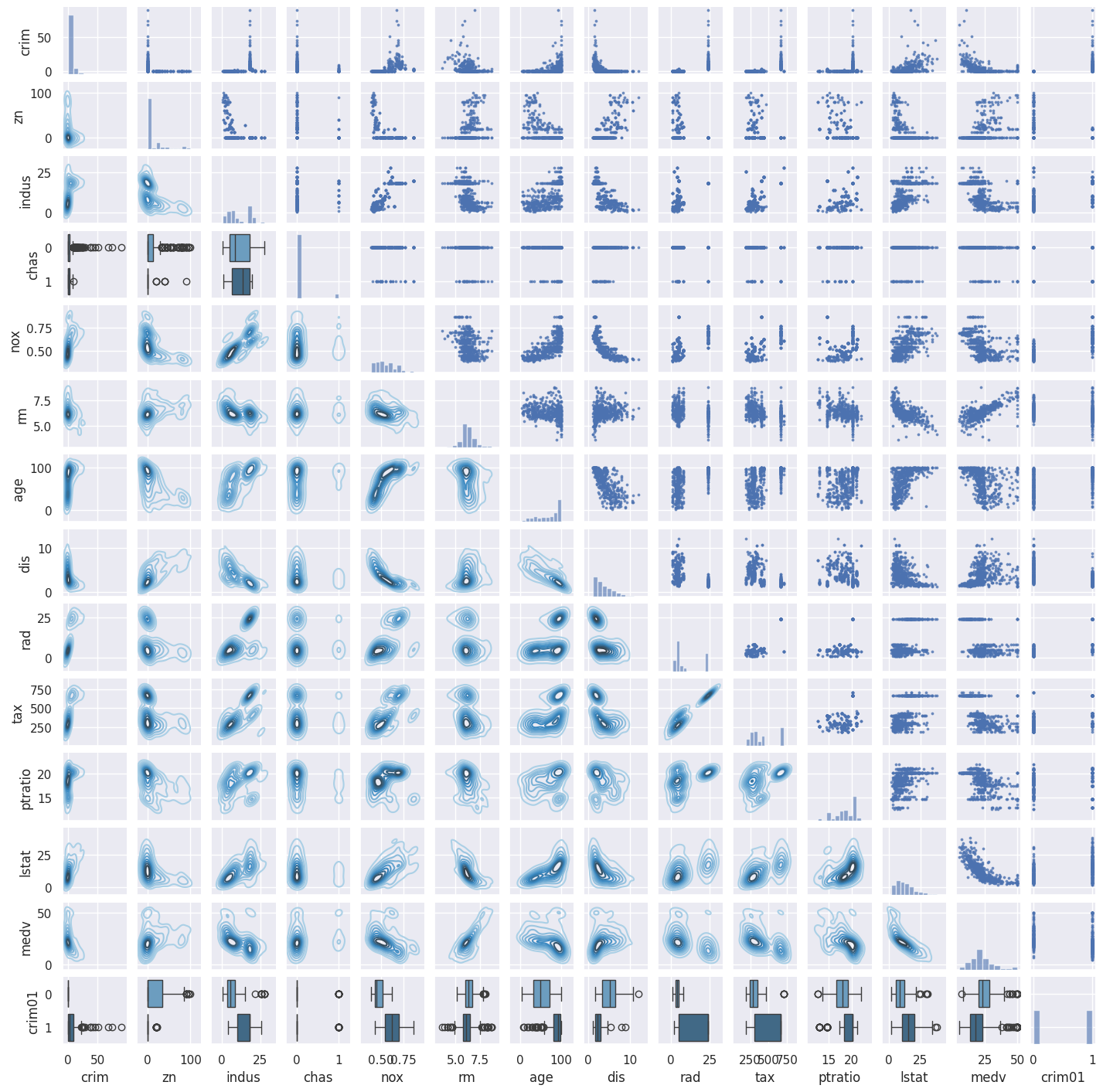

g = sns.PairGrid(boston)

g.map_upper(plt.scatter, s=3, alpha=0.7)

g.map_diag(plt.hist, alpha=0.6)

def lower_plots(x, y, **kwargs):

if y.name in ['crim01', 'chas']:

num_colors_needed = y.nunique()

sns.boxplot(x=x, y=y, orient='h', hue=y, palette=sns.color_palette('Blues_d', n_colors=num_colors_needed), **kwargs) # Horizontal boxplot

else:

sns.kdeplot(x=x, y=y, cmap='Blues_d', **kwargs) # KDE plot

g.map_lower(lower_plots)

g.figure.set_size_inches(14, 14);

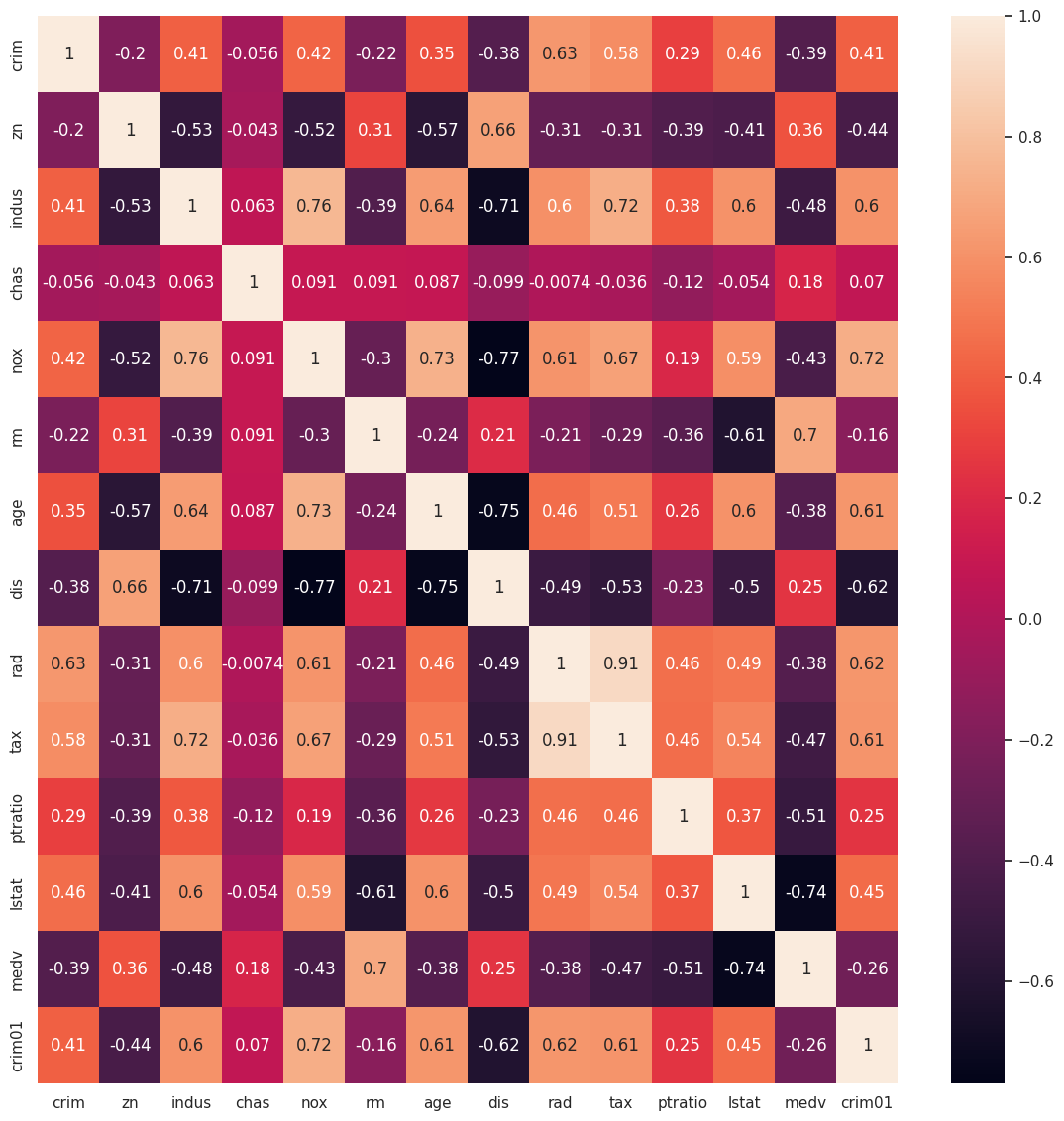

plt.figure(figsize=(14, 14))

sns.heatmap(boston.corr(), annot=True);

Looking at the heatmap and the plots, I decided to use the variables indus, nox, age, dis, rad, tax because seem to have strong relationships with crim01.

X = boston[['indus', 'nox', 'age', 'dis', 'rad', 'tax']]

y = boston['crim01']

def fit_and_get_error_rate(model, X, y):

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.3, random_state=1)

mdl = model

mdl.fit(X_train, y_train)

pred = mdl.predict(X_test)

conf_mat = confusion_table(pred, y_test)

return get_error_rate(conf_mat)

Using the function above on the 4 models to fit them and get their error rates:

for model in [LDA(), QDA(), LogisticRegression(max_iter=1000), GaussianNB()]:

print(f'{model.__str__().split("(")[0]}: {fit_and_get_error_rate(model, X, y)}\n')

LinearDiscriminantAnalysis: 0.17763157894736842

QuadraticDiscriminantAnalysis: 0.125

LogisticRegression: 0.17763157894736842

GaussianNB: 0.19078947368421054

We can see the test error rate for each of the models and see that QDA performed the best here with a test error rate of 12.5%.

Now to fit the KNN classifier we’ll start by standardizing the data.

scaler = StandardScaler(with_mean=True,

with_std=True,

copy=True)

X_std = scaler.fit_transform(X)

feature_std = pd.DataFrame(

X_std,

columns=X.columns);

feature_std.std()

indus 1.00099

nox 1.00099

age 1.00099

dis 1.00099

rad 1.00099

tax 1.00099

dtype: float64

X_train_std, X_test_std, y_train_std, y_test_std = train_test_split(feature_std, y, test_size=0.4,random_state=1)

error_rate = {}

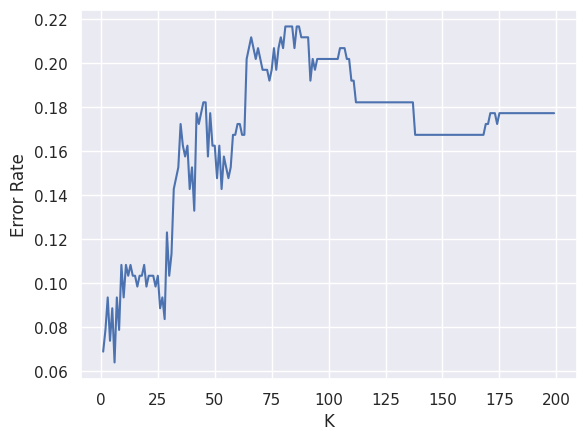

for k in range(1, 200):

knn = KNeighborsClassifier(n_neighbors=k)

knn.fit(X_train_std, y_train_std)

knn_pred = knn.predict(X_test_std)

conf_mat = confusion_table(knn_pred, y_test_std)

error_rate[k] = get_error_rate(conf_mat)

plt.plot(error_rate.keys(), error_rate.values())

plt.xlabel('K')

plt.ylabel('Error Rate');

k_min = min(error_rate, key=error_rate.get)

k_min, error_rate[k_min]

(6, 0.06403940886699508)

K = 6 seems to be the best value for the KNN classifier with a test error rate of 6.4%.